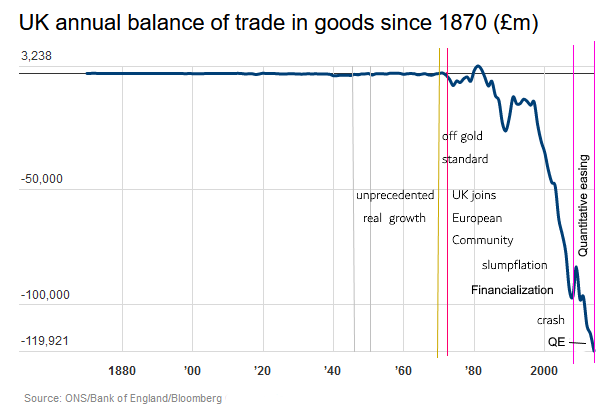

The hard data recorded in graphical form on the left spells out the decadence in this county's trade in goods performance since three unfortunate decisions were taken in 1971, 1973 and 1975 and which set in motion trends which hollowed out the UK's manufacturing sector competitive status culminating in the 2008 financial crisis. These were coming off the Gold Standard, joining the EU and switching to the monetarist paradigm. For a broader treatment on these issues see,

"Bretton Woods in retrospect".

It has been revealing to accompany some of the evidence provided by the Secretary of State for International Trade to parliamentary committees. In these exchanges occasionally the Secretary's previous role as Minister of State for Business, Energy and Clean Growth can be seen to have been useful. However, throughout these proceedings there is never any questioning of our current macroeconomic policies and their impact on trade competitivity.

The Conservatives have a tendency to be skeptical of industrial policies on the basis that civil servants and politicians are in no position to make decisions that need to be taken by private business. This is quite reasonable but if the macroeconomic policies have the effect of constraining decision-making in the private sector this valid argument is undermined.

Real Incomes Policy

RIP has two macroeconomic policy instruments:

The PPR is a measure of progress of each economic unit in lowering the ratio between changes in output prices against variations in input costs. The PPL is a rebate on a basic levy according to the PPR values achieved. Economic units can manage their affairs to minimize the levy even to zero. In this way the macroeconomic policy is coordinated by the participatory development of companies and their work forces and not by largely arbitrary interest and debt targets. RIP bases policy impact and success on the knowledge and calculations made by the economic actors thereby solving the calculation and knowledge problem in an operational structure that more closely approximates participatory constitutional economics.

|

|

|

A need for a constitutional economicsIn spite of the diminished size of our industrial sector there remain immense variations in capabilities and conditions of sector participants. This signifies that it is necessary to have a macreconomic policy that steers clear from state dictats in the shape of macroeconomic policy instrument setting by the Bank of England in support of government objectives. These dictats serve the objectives which the Bank of England cannot in reality control. The declared objectives are "price stability" and a target inflation rate of 2% "supported" by the policy instrument of base interest rates and drawing on the additional "support" of government setting of fiscal policy taxation rates. This target inflation rate represents a 18% devaluation of the currency and real incomes each decade. Quantitative easing (QE), during the last 12 years, has accelerated the decline in supply side production investment and productivity because of a diversion of QE finds into offshore investments and assets (for further details see the document,

"Why monetarism does not work"). Since this has a direct impact on national industrial and trade competitivity and the national cost of living and UK's bargaining position in any trade negotiations, this is something any trade officials and policy makers should be concerned about.

As it is policy ignores the essential requirement for central policies to respond to the specific conditions of each economic unit (see,

"RIP and the calculation & knowledge problem" and also,

Ludwig von Mises' calculation and knowledge problem revisited). The failure to do this results in policy creating winners, losers and some in a policy-neutral impact state. Conventional policies require a go-stop policy regime which in itself is destabilizing.

To create a policy that supports all, a constitutional approach would enable economic units respond to any economic conditions to comply with their specific capabilities and conditions. Real Incomes Policy (RIP) avoids the go-stop approach by establishing an incentive scheme to encourage investment in productivity enhancing change to generate immediate higher returns associated with price moderation and profits associated with higher rates of national and international market penetration.

Whether innovation is strictly linked to physical productivity, costs reduction, unit price reduction, profits or wages it will, under RIP, also provide the foundation for increasing sustainability and address necessary climate change actions to achieve more for less.

1 Hector McNeill is director of SEEL-Systems Engineering Economics Lab

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2021) unless otherwise indicated