The Transactional and Hedging Model

The Black & Scholes Model

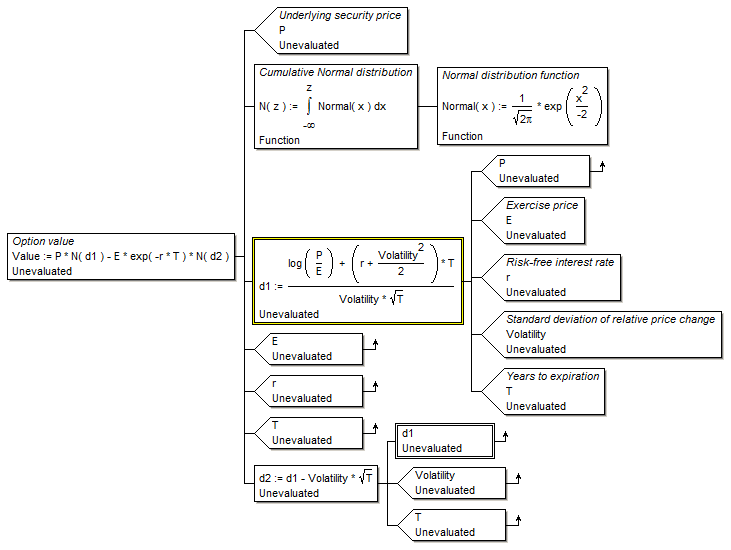

The diagram below shows the Black & Scholes model built in DScript and used to determine fundamental decision risks in a real market envelope. Several real factors that affect intrinsic value are not included in the model and it can therefore fail without warning.

A more robust model (SEEL-TTT1) takes into account all real market envelope determinants in real time and can therefore track trends more precisely and predict sharp shifts.

Seel-Telesis Project, 2003.

1 TTT-Transactional Trading Terminals, a division of VisualModel.com |

|

|

Front End Loading & the Bonus Culture

Hector McNeill

SEEL

I first came across the concept of "front end loading" in the early 1980s when I was providing investment consultancy to six leading investment groups based in the City of London. My work involved identifying investment opportunities and then evaluating them in terms of technical, economic, financial and environmental returns and impacts. With my first submission of proposals I was asked why I had not made provisions for front end loading. When I asked what this meant, I was informed that the investment group needed to take their "profit" on the "sale" of the investment. Indeed, I was informed that, unless the investment proposals contained such provisions they would not be submitted to the boards of the different groups concerned. I had received my training in project identification, preparation and evaluation at Cambridge University where we used case studies of World Bank projects. Part of this work included investment project sensitivity analysis as a basis for assessing risk and the likelihood of the evolving quantified returns in the form of profit over and above cash flow items arising from the future streams. Naturally future income streams would only be available once the investment had been implemented and had become operational. Therefore profit was considered to be a downstream benefit. I explained these details but was informed that the future cash flow arising from the investment performance was secondary to the specific interest in structuring the "sales package" for the investment, to make sure the investment groups made their profit on the act of sale. This also meant that any short term profit going to their clients (investors) would be correspondingly reduced. The investment fund managers were more interested in a sales commission than in anything related to real performance. They were not only financializing the investment they were commoditizing it into an object to be sold like apples, cars or a house. Future income streams and performance were to become the responsibility of whoever purchased the package. This is why, cancelling an insurance policy within one or two years of initiating it, one can expect to get back less than 20% of what was paid in. The financial intermediaries have all sorts of ways of explaining this such as "administrative costs".

Investment fund managers therefore will look at a large part of their portfolio as objects upon which they wish to make a high profit for very little investment of their own funds. It is the movement or transaction of investment packages, including derivatives, where the main profit incentive exists.

The spread in portfolios also relates to uncertainty of the performance of each object and "hedging" becomes an important activity to guard against intrinsic value changes in the objects. These objects also known as options or derivatives are not a new phenomenon but their contemporary form appeared in the 1970s. A model that attempted to explain the relationship between options and hedging was developed by Fischer Black and Myron Scholes in a paper published in 1973 entitled,"The Pricing of Options and Corporate Liabilities." They developed a partial differential equation that estimates the price of an option over time. The objective of the model was to perfect option hedging by buying and selling the underlying asset at the right time and price so as to sustain a position of "risk elimination". Indeed, this basic model has been used by investment banks. The problem with the model is that it assumes less extreme price changes than can occur in reality, when confidence declines because of perceived or real "re-valuations". Many suffered from this weakness during the October 1987 crash when the Dow Jones index dropped 23% in a single day and then again in 2007 with sub-prime derivatives tipped into value decline when the Federal Reserve's raising of interest rates that November.

The rampant failures in the Black & Scholes model are caused by its dependency upon the classic supply and demand equilibrium model geared to determining the "risk" of price movements of financialized and commoditized objects (options or derivatives) as opposed to taking into account the underlying and intrinsic values of objects generating cash flow. These values cannot be estimated using Black & Scholes and the whole "play" and hedging positions are determined by assumed market trends and relative stability. While there is relative stability (for whatever reason) hedging can not only reduce momentary risk but also generate profits which the model is used to trigger computer-based trades, literally within a second of relative price movements. However, this activity has little to do with fundamental moves in commodity supply or derivative quality, that is, "fundamentals". It is more to do with using devices to front end load any transaction like the investment groups referred to at the beginning of this article.

The outcome is that a significant part of trading positions are not adding value for those in the market but is permitting the skimming of margins off the normal positions within the market.

One only has to reassess Black & Scholes against a Real Incomes costs and purchasing power envelope to see that it only works under high confidence and where this is not wholly related to real option performance but rather perceived performance.

People working in this environment have a natural tendency to confuse sales volumes with performance, or rather, to see sales values as the bottom line to performance. As a result executive bonuses are related to short term sales of commoditized derivatives even although what is being sold is a loan or an investment, with a medium to long term performance which should be the determinant of income and bonuses. As a result the emphasis on front end loading has led to a somewhat irresponsible attitude to real value where sales packaging and rating labels have substituted ethical decision analysis based upon objective life cycle investment analysis; it is as if there were no future or no obligation to the younger generation who will inherit this pernicious legacy.

|